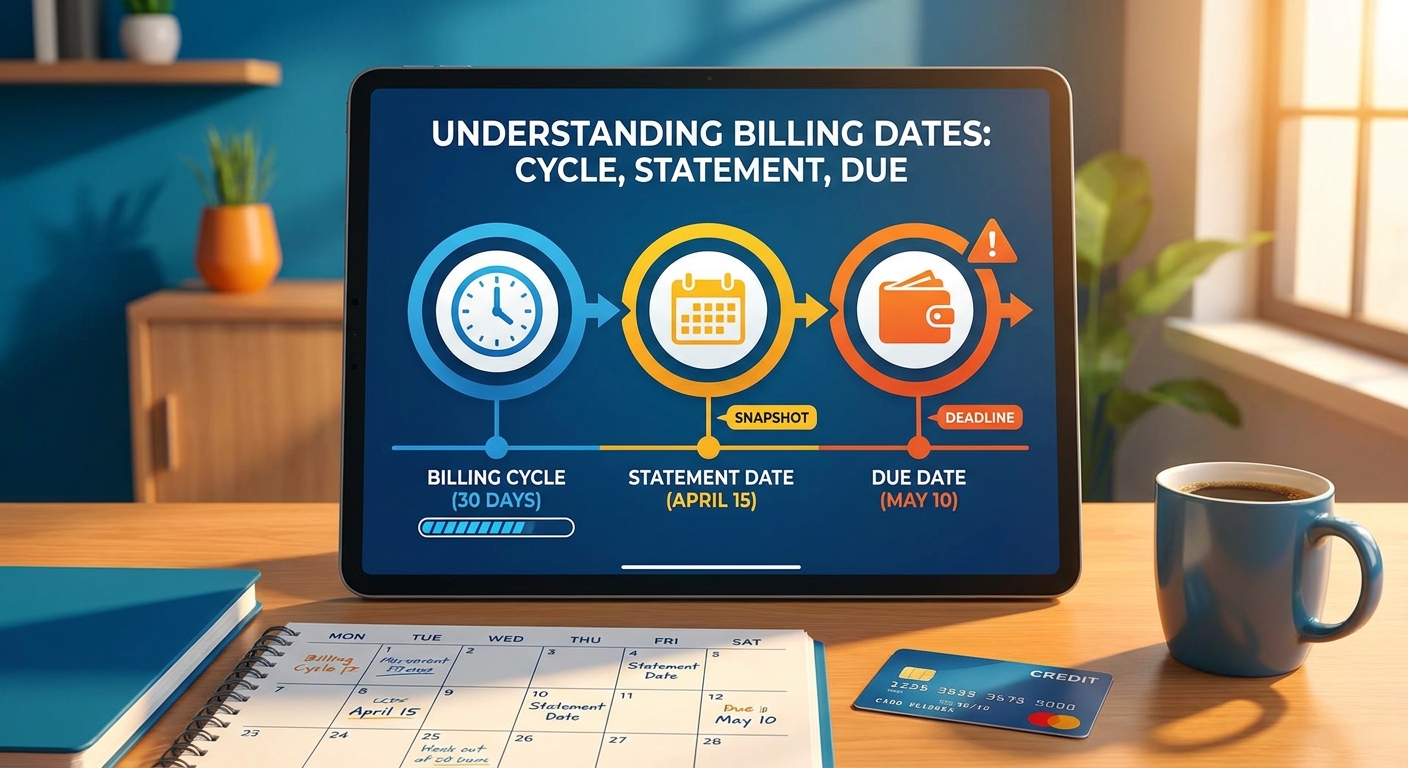

Billing Cycle, Statement Date, and Due Date: Why All Three Matter

Have you ever looked at your credit card statement and felt a bit like you needed a decoder ring? You’re not alone! Many credit card users find themselves puzzled by terms like "billing cycle," "statement date," and "due date." While they might seem like mere technicalities, understanding these three crucial dates is fundamental to smart credit card management, avoiding unnecessary fees, and protecting your financial health. Think of them as the three pillars supporting your responsible credit card use. Ignore one, and the whole structure can wobble.

In this comprehensive guide, we'll demystify these terms, explain how they work together, and show you why knowing them inside and out is one of the best financial habits you can cultivate. Let's dive in and turn confusion into clarity!

The Billing Cycle: The Foundation of Your Credit Card Activity

Let's start at the beginning. The billing cycle, sometimes called the "statement period," is simply the period of time between two consecutive statement dates. Most credit card billing cycles last between 28 and 31 days, though the exact length can vary slightly from one month to the next due to the varying number of days in a calendar month.

How the Billing Cycle Works

Imagine your credit card company drawing a line in the sand. All transactions (purchases, cash advances, balance transfers, and even returns or payments) made during this specific period are grouped together and appear on your next credit card statement. Once the cycle ends, a new one immediately begins.

- Starts: Typically the day after your previous statement date.

- Ends: On your current statement date.

- What it captures: All financial activity on your account within that specific timeframe.

Understanding "what is a billing cycle" is crucial because it dictates which purchases will appear on your current statement and, therefore, which ones will be subject to payment by your due date. Purchases made early in a cycle might give you nearly two months before payment is due, whereas purchases made late in a cycle will have a much shorter window.

The Statement Date: Your Monthly Financial Snapshot

The statement date, also known as the "closing date" or "cycle close date," is the day your billing cycle officially ends, and your credit card issuer generates your monthly statement. This date is fixed and typically falls on the same calendar day each month (e.g., the 15th of every month).

What Your Statement Date Reveals

On your statement date, your credit card company calculates everything that happened during the preceding billing cycle. This includes:

- Your outstanding balance from the previous cycle.

- All new purchases and other charges.

- Any payments you've made.

- Applied interest charges (if applicable).

- Any fees incurred (like late payment fees).

The sum of all this activity becomes your "statement balance" – the total amount you owe for that specific billing cycle. The statement date is your financial snapshot; it’s the definitive record of your account activity up to that point. The balance reported on this date is also often what gets reported to credit bureaus, impacting your credit utilization ratio.

The Due Date: The Deadline That Truly Matters

Finally, we have the due date. This is the absolute last day your credit card company must receive your payment to avoid late fees and interest charges. It's usually a specific number of days (typically 21-25) after your statement date.

Why the Due Date Is Non-Negotiable

The due date is arguably the most critical of the three dates for your immediate financial health and credit score. Missing it carries significant consequences:

- Late Fees: You'll almost certainly be charged a late fee, which can be substantial.

- Interest Charges: If you don't pay your full statement balance by the due date, you'll lose your interest-free "grace period." This means interest will be charged on your outstanding balance, and often, on new purchases from the moment they are made, until you pay off the full balance.

- Credit Score Damage: Payments reported 30 days or more past due can severely damage your credit score, making it harder to get loans, mortgages, or even rent apartments in the future.

- Penalty APR: Some cards may impose a higher penalty Annual Percentage Rate (APR) if you miss a payment, which can last for several billing cycles.

It’s vital to distinguish between paying the "minimum payment due" and paying the "full statement balance." While paying the minimum prevents late fees and credit score damage, paying the full statement balance is the only way to avoid interest charges and maintain your grace period on new purchases.

Why All Three Matter: The Interconnected Web of Your Credit Card

Now that we've defined each term, let's connect the dots. The power (and potential peril) lies in how the billing cycle, statement date, and due date interact.

Maximizing Your Grace Period and Avoiding Interest

This is perhaps the most significant reason to understand these dates. Most credit cards offer an interest-free "grace period" on new purchases. This means if you pay your full statement balance by the due date, you won't be charged interest on those new purchases. The grace period typically starts on your statement date and ends on your due date.

- Scenario 1: You pay your full statement balance. You enjoy the grace period. Any new purchases made *after* your statement date (i.e., in the new billing cycle) will not accrue interest until the *next* billing cycle's due date, provided you continue to pay in full.

- Scenario 2: You pay only the minimum or less than the full statement balance. You lose your grace period. Interest will be applied to your remaining balance from the statement date. Crucially, new purchases made during the *current* billing cycle (even after the statement date of the *previous* cycle) will typically start accruing interest immediately, from the transaction date, until your entire balance is paid off. This is where many people get caught out!

Strategic Spending and Budgeting

Knowing your billing cycle helps you plan larger purchases. For instance, if you make a big purchase right at the beginning of a new billing cycle, you'll have almost two months before that specific purchase appears on a statement and is then due. Conversely, a purchase made near the end of a billing cycle will be due much sooner.

Protecting and Improving Your Credit Score

Paying on time, every time, is the biggest factor in maintaining a good credit score. Understanding your due date ensures you never miss a payment. Additionally, the balance reported to credit bureaus is often your statement balance. If you're trying to reduce your credit utilization (the amount of credit you're using compared to your total available credit), making a payment *before* your statement date can result in a lower balance being reported, which is beneficial for your score.

Effective Financial Planning

Aligning your payment due dates with your paychecks can simplify your budgeting. If your paychecks land mid-month, and your credit card due date is the 1st, you might find yourself struggling to pay on time. Many card issuers allow you to change your due date, which can be a valuable tool for managing credit card due dates more effectively.

Best Practices for Managing Your Credit Card Dates

Taking control of these dates is simpler than you might think. Here are some actionable tips:

- Locate Your Dates: Your billing cycle, statement date, and due date are clearly listed on every monthly credit card statement. Make a point to find them.

- Set Up Auto-Pay: To ensure you never miss a due date, set up automatic payments for at least the minimum amount. Ideally, set it to pay your full statement balance.

- Use Reminders: Calendar alerts, banking app notifications, or even sticky notes can serve as excellent reminders for your due date. Consider setting one a few days before the actual due date to allow processing time.

- Review Your Statements: Don't just pay; review. Check your statement balance against your own records, look for unauthorized charges, and understand where your money is going. This also helps you track your statement closing date meaning and how it impacts your payments.

- Pay More Than the Minimum: Always strive to pay your full statement balance. If you can't, pay as much as you possibly can above the minimum to reduce interest charges.

- Consider Changing Your Due Date: If your current due date doesn't align well with your income, contact your credit card issuer. Many are happy to adjust it for you.

Conclusion: Empower Yourself Through Knowledge

The billing cycle, statement date, and due date aren't just arbitrary numbers on your credit card statement; they are the gears that drive your credit card's financial machinery. By understanding how each piece works and, more importantly, how they interrelate, you gain powerful control over your spending, interest payments, and credit score. This knowledge is key to managing credit card due dates effectively and avoiding the financial implications billing dates can have if misunderstood.

Take the time to pinpoint these dates for all your credit cards, integrate them into your financial routine, and transform passive credit card use into active, informed financial management. Your wallet and your credit score will thank you!

Stay informed and master your finances! Subscribe to our newsletter for more expert insights and tips delivered straight to your inbox.

References & Sources

Consumer Financial Protection Bureau (CFPB) - How does the grace period work on a credit card?

Experian - What Is a Credit Card Billing Cycle?

Investopedia - Credit Card Billing Cycle: Definition, How It Works, and Dates